-

economicmargins

-

February 5, 2026

February 5, 2026 -

Global Economy

Global Economy

Sri Lanka’s Economic Odyssey: The Rise, the Fall, and the Remarkable Return

Sri Lanka, an island nation in South Asia, has historically been regarded as a moderately stable economy with potential for growth due to its strategic location, diversified agricultural base, and tourism appeal. However, it suffered the most severe economic crisis in its post-independence history, though it has again been able to rebound its economic activities so far.

Before the Crisis: A “Development Success Story”

With a threefold increase in GDP per capita in purchasing power parity (PPP) over 25 years, Sri Lanka moved from the classification of a low-income country (LIC) to a lower-middle-income country (LMIC) in 1997, before reaching the status of an upper-middle-income country (UMIC) in 2018. Furthermore, the country managed to virtually eliminate extreme poverty, boasting high literacy rates (92% of adults), life expectancy (76 years), and low infant mortality (7‰). Sri Lanka ranked 73rd out of 191 countries in the 2021 UN Human Development Index (HDI), well ahead of its South Asian neighbors.

Annual growth averaged almost 6% between 1993 and 2017 as a result of liberalization measures initiated in 1990, followed by the end of the civil war in 2009. Growth was primarily fostered by the service sector, which accounted for more than 50% of the economy, followed by manufacturing (around 20%) and agriculture (around 10%). As the country enjoys a favorable geographic position and invested heavily in transport and logistics activities in an effort to become a regional hub (Colombo is one of the three largest ports in South Asia in terms of container volume handled), the growth of the tourism industry contributed significantly to the service sector. The agrifood industry (especially tea processing) and the textile industry contributed to the manufacturing sector. The construction industry, largely dependent on public procurement and major projects, also contributed to growth. Throughout this period, the growing expatriation of Sri Lankan workers to Western countries and later to Gulf countries significantly boosted household consumption through substantial remittances.

However, the economy inherited significant structural imbalances.

Since the 1990s, Sri Lankan government revenue relative to GDP has been on a downward trend and has remained among the lowest in the world. It stood at only around 12% of GDP during the 2010s, far below the South Asian average of 21%, primarily due to a narrow tax base, low tax rates, numerous exemptions, tax evasion, and the lack of productivity in public enterprises. Public spending was higher, reaching 18% of GDP during the same period. The interest burden and the payroll for more than a million public servants (15% of the working population) alone absorbed three-quarters of government revenue. At the same time, investment expenditure and security expenditure were also substantial. As a result of the shortfall in revenue to cover expenditure, public accounts remained structurally imbalanced. During the 30 years prior to the crisis, the fiscal deficit consistently remained above 5% of GDP.

At the same time, between 2008 and 2017, strong economic growth made it possible to maintain public debt at around 70% of GDP, but there was a shift in the type of the country’s external creditors. Historically, Sri Lanka primarily relied on flows from multilateral donors and Paris Club countries. From the late 2000s onward, these donors were gradually replaced by Chinese loans and international foreign-currency bonds (Eurobonds). These private flows, which are more costly, have also been much more volatile and sensitive to the economic climate.

Economic Crisis (2019–2024)

Sri Lanka’s economic crisis (2019–2024) represents one of the most severe and multidimensional economic collapses in recent South Asian history, manifested through hyperinflation, currency depreciation, severe shortages of essential goods, declining foreign reserves, and social unrest.

Key indicators illustrate the severity of the crisis. By 2022, the Sri Lankan rupee had depreciated by over 50% against the US dollar, the economy contracted by 7.3%, inflation peaked at nearly 70%, and foreign reserves fell to critically low levels—just enough to cover 1.2 months of imports in 2022. These factors triggered widespread public dissatisfaction, culminating in large-scale protests and the resignation of both the President and Prime Minister in mid-2022.

Causes of the Crisis

Sri Lanka’s economic crisis was not the result of a single factor but rather a convergence of fiscal mismanagement, external shocks, and policy failures. Each of these factors interacted in complex ways, magnifying the severity of the crisis. This section explores these causes in detail.

Fiscal Mismanagement

Fiscal mismanagement has been widely regarded as the primary driver of Sri Lanka’s economic collapse.

Tax Cuts and Revenue Decline

In late 2019, the government implemented sweeping tax reforms, including the reduction of the Value Added Tax (VAT) from 15% to 8%, cuts to corporate taxes, and the removal of several indirect taxes. These tax reforms caused government revenue to fall by approximately 33% in the first year alone (according to the Central Bank of Sri Lanka). This reduction in revenue left the government unable to finance essential public services, including healthcare, education, and social welfare programs, without resorting to borrowing or monetary expansion.

Unsustainable Borrowing

To cover the fiscal deficit, Sri Lanka relied heavily on both domestic and international borrowing. Between 2019 and 2021, Sri Lanka’s public debt rose from $55 billion to $84 billion (from 83% of GDP to 120%), with external debt comprising nearly 60% (around $51 billion) of the total debt. Much of this debt was used to finance large infrastructure projects such as the Hambantota Port, Mattala Airport, and the Lotus Tower, which were politically motivated but economically unviable and failed to generate expected returns.

High-interest loans from foreign governments and institutions increased debt-servicing costs, consuming nearly 40% of government revenue by 2021, including borrowing through Eurobonds. By the end of 2022, Sri Lanka had to repay around US$4 billion in debt, while government reserves amounted to only US$2.3 billion as of April 2022. As a result, the country was forced to default on approximately US$51 billion of external debt for the first time in its history. Unsustainable borrowing to finance projects without proper cost-benefit analysis ultimately led to the crisis.

Lack of Monetary Authority Independence

In an attempt to bridge fiscal gaps, the Central Bank increased the money supply through currency printing (a practice known as monetary financing), bypassing fiscal discipline and directly fueling hyperinflation. By mid-2022, inflation peaked at nearly 70%, severely eroding purchasing power and causing the prices of essential commodities such as rice, cooking oil, and fuel to soar.

The Central Bank of Sri Lanka (CBSL) maintained an artificial peg of the Sri Lankan rupee (LKR) at approximately 200 per USD despite dwindling foreign reserves. The bank sold dollars to defend the non-credible peg, which depleted usable reserves. Later, the depreciation of the Sri Lankan rupee (over 50% against the US dollar in 2022) compounded the problem, increasing import costs and worsening the trade deficit.

External Shocks

While fiscal mismanagement created vulnerability, external shocks triggered and intensified the crisis.

COVID-19 Pandemic

The tourism industry (which contributed around 5% of Sri Lanka’s GDP pre-pandemic), already severely affected by the Easter bombings of 2019, further collapsed due to global travel restrictions. Remittances from overseas workers also declined by about 20% in 2020, reducing a critical source of foreign exchange for the country. Exports of tea and garments faced disruptions in global supply chains, further weakening the balance of payments.

Global Commodity Price Shocks

The Ukraine conflict in 2022 caused global spikes in oil and food prices, disproportionately affecting Sri Lanka due to its dependence on imported fuel and food. The country’s fuel import bill doubled within months, straining already limited foreign reserves. The rise in global fertilizer prices, combined with domestic bans on chemical fertilizers, led to severe reductions in crop yields and increased food insecurity.

Natural Disasters

Sri Lanka faced adverse weather events, including floods and droughts, which further disrupted agricultural output. These environmental shocks magnified the food supply crisis and increased public discontent, creating a vicious cycle of economic stress and social unrest.

Policy Failure

Several domestic policy decisions exacerbated the economic collapse, highlighting systemic weaknesses in governance and planning.

Agricultural Policy

The government imposed a sudden ban on chemical fertilizers in 2021 to promote organic agriculture, despite the initial plan for phased implementation. Rice and vegetable production dropped drastically, and the paddy harvest declined by approximately 20% in 2021–2022. The policy led to shortages of staple foods, sharply increasing prices and fueling inflation, while failing to provide adequate organic alternatives. Tea, a major agricultural export, was also severely impacted due to rising production costs coupled with low productivity.

Energy Sector Mismanagement

Subsidies on fuel were maintained despite skyrocketing global oil prices, leading to severe fiscal strain. Public sector inefficiencies in distribution created long queues and black-market fuel trading, which became a source of public anger and social unrest.

Debt Negotiation and Governance Failures

Failure to negotiate debt restructuring early in the crisis meant that by 2022 Sri Lanka faced insurmountable repayment obligations, forcing the country to default. Policy decisions were often reactive rather than proactive and lacked long-term strategic planning, which deepened both economic and social consequences.

Social and Economic Impact

The combination of fiscal mismanagement, external shocks, and policy failures led to profound social consequences:

- Widespread shortages: Scarcity of essentials such as food, fuel, and medicines led to rationing and public panic.

- Inflation and purchasing power: Hyperinflation caused a severe decline in real income, pushing over 30% of the population into poverty.

- Unemployment: Business closures and industrial slowdowns increased unemployment, especially among young adults.

- Protests and political instability: Citizens protested against rising prices and shortages, culminating in the resignation and fleeing of the President in July 2022.

Fiscal mismanagement made the economy vulnerable to external shocks, while poor policy decisions amplified the social consequences.

Recovery Path

After a catastrophic economic collapse marked by sovereign default, high inflation, and political upheaval, Sri Lanka embarked on an IMF-led recovery path with combined monetary and fiscal reforms. This led the country to achieve notable progress in restoring macroeconomic stability and rebuilding confidence.

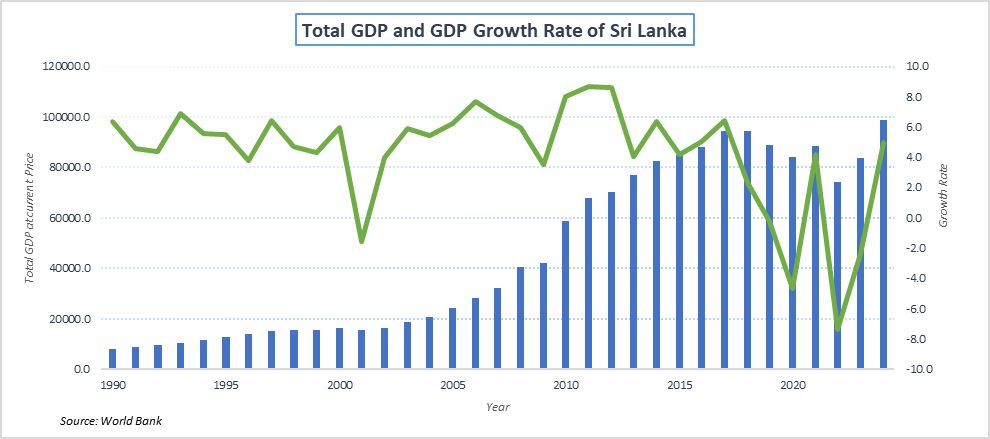

The economy grew by about 5% in 2024 after consecutive negative growth in the previous two years and is expected to grow by 3–5% in the coming years. Inflation, which had reached 70%, has fallen to below 5%. The rupee has remained relatively stable in recent months, and foreign exchange reserves have surged, tripling their import cover from one month at the end of 2022 to three months by mid-2025. The external current account has remained in surplus for a second consecutive year. Credit rating agencies have upgraded the country’s rating. Extremely low government revenues have increased from 8.4% of GDP in 2022 to an expected 15% in 2025, leading to a projected primary surplus of 2.2% of GDP in 2025.

Reform Initiatives for Stability

In response to the economic crisis, Sri Lanka implemented a combination of international assistance programs, domestic fiscal and monetary reforms, and structural adjustments that helped stabilize the economy.

IMF Bailout Program

In March 2023, the International Monetary Fund approved a four-year, $3 billion Extended Fund Facility (EFF) to help Sri Lanka stabilize its economy. The program required fiscal consolidation measures, including broadening the tax base and reducing subsidies, reforming state-owned enterprises to improve efficiency, and strengthening transparent governance and anti-corruption measures.

The program provided immediate liquidity support, helped avert the total collapse of essential services, encouraged bilateral creditors and investors to engage in debt restructuring discussions, and helped restore international confidence and unlock funds from other lenders.

Debt Restructuring

Deals were reached with major bilateral lenders such as India, China, and Japan to extend repayment periods and reduce debt pressure. The government introduced “Governance-Linked Bonds,” a global first where interest rates are tied to the country meeting specific governance and anti-corruption targets for private bondholders. The government also restructured domestic debt, though this primarily affected pension funds such as the Employees’ Provident Fund (EPF).

Fiscal Reforms (Tax Increases)

Reintroduction and adjustment of VAT (from 8% to 15%) and corporate taxes, along with income tax increases for higher earners, helped raise government revenue. Gradual reductions in fuel and fertilizer subsidies aligned domestic prices with global market rates. Government spending was redirected toward essential social services and debt repayment. Through these measures, the government was able to achieve a primary fiscal balance.

Monetary and Exchange Rate Reforms

Sri Lanka passed a new law to strengthen the independence of the Central Bank of Sri Lanka. The Central Bank increased policy rates to curb hyperinflation and made efforts to reduce rupee volatility by intervening in foreign exchange markets and securing IMF and bilateral funding.

Structural Reforms

The government-initiated reform measures for state-owned enterprises to reduce inefficiencies and improve profitability. Promotion of export-oriented industries such as tea, apparel, tourism, and IT services was prioritized. Overseas workers were encouraged to send more remittances to boost foreign exchange earnings. Policies were also introduced to encourage foreign direct investment (FDI), including tax incentives and simplified regulatory procedures.

Import restrictions and foreign exchange controls on luxury goods, along with prioritization of essential imports such as fuel, medicine, and food, helped maintain scarce foreign currency reserves within the economy.

Bilateral and Multilateral Support

India provided over $4 billion in assistance, helping Sri Lanka avoid a complete collapse in imports. The World Bank and the Asian Development Bank offered emergency grants and low-interest loans to stabilize the healthcare, agriculture, and energy sectors.

Challenges Ahead

Despite these improvements, several challenges remain. Public debt levels remain extremely high, and while the current restructuring provides breathing room, a significant “step-up” in interest payments begins in 2028. Sri Lanka must achieve strong growth now to afford those future obligations.

Fiscal reforms, including higher taxes and reduced public spending, have been politically unpopular and have placed a burden on households. Poverty levels increased significantly during the crisis, reaching around 25% of the population, and the cost of living has risen.

Additionally, several state-owned enterprises continue to operate at a loss, requiring government subsidies that further strain public finances.

Economic recovery remains slow, and restoring investor confidence and stimulating private investment remain challenging. Sri Lanka is also highly vulnerable to climate risks; a catastrophic cyclone in late 2025 caused over 600 deaths and massive infrastructure damage, making the recovery path more difficult. As Sri Lanka’s economy is heavily dependent on remittances and tourism earnings, evolving geopolitical tensions and unpredictable global policies remain major threats to its fragile economy.

Conclusion

Sri Lanka has stabilized its economy through growth, lower inflation, stronger reserves, and debt restructuring, while launching an anti-corruption drive. However, poverty remains high, reforms are incomplete, and climate shocks can quickly reverse progress, adding pressure on governance and resilience. Recovery requires strategic, coordinated, and long-term efforts to restore stability and foster sustainable growth.

Growth-led development must be the main economic strategy. IMF-supported programs and debt restructuring provided immediate relief but must be complemented by long-term structural reforms. Fiscal discipline, monetary prudence, and diversification of exports are essential for future economic resilience. Strengthening governance, transparency, and public accountability is required to prevent policy missteps and enhance social stability.

In conclusion, Sri Lanka’s experience serves as a cautionary tale for emerging economies. It demonstrates that delays in structural reforms in favor of populist fiscal policies can turn manageable external shocks into a systemic economic collapse.

Bibliography

Asian Development Bank (ADB). (2023). Asian Development Outlook 2023: Sri Lanka Economic Update. Manila: ADB.

Central Bank of Sri Lanka. (2022). Annual Report 2022. Colombo: Central Bank of Sri Lanka.

Food and Agriculture Organization (FAO). (2022). Impact of Fertilizer Ban on Agricultural Production in Sri Lanka. Rome: FAO.

International Monetary Fund (IMF). (2023). Sri Lanka: Request for an Extended Arrangement under the Extended Fund Facility. Washington DC: IMF.

United Nations Development Programme (UNDP). (2021). Human Development Report 2021/2022. New York: UNDP.

World Bank. (2022). Sri Lanka Development Update: Protecting the Poor and Vulnerable in a Time of Crisis. Washington DC: World Bank.

World Bank. (2023). Sri Lanka Macro Poverty Outlook. Washington DC: World Bank.

International Crisis Group. (2023). Sri Lanka’s Economic Crisis and Political Transition. Brussels: International Crisis Group.